{kind=link}

Checking your credit score regularly is an important part of your financial health. Your credit score helps you gauge how creditors will view your credit if you decided to apply for a credit card or loan in the near future.

What is a Credit Score?

Credit scores are a three-digit number calculated based on the information in your credit report. You probably know that having a higher credit score is better, but it’s hard to know exactly what your credit score means if you don’t have something to put it into perspective. Knowing the credit score rating scale range helps you figure out whether your specific credit score is good or bad.

There are many different credit scoring models, FICO Score and the Vantage Score are the two most commonly used and well-known credit scores. When you apply for credit, the lender is most likely to use one of those two credit scores. The latest versions of the FICO and VantageScore fall on a range of 300 to 850. Credit scores on the higher end of the range are considered good and those on the lower and of the range are bad.

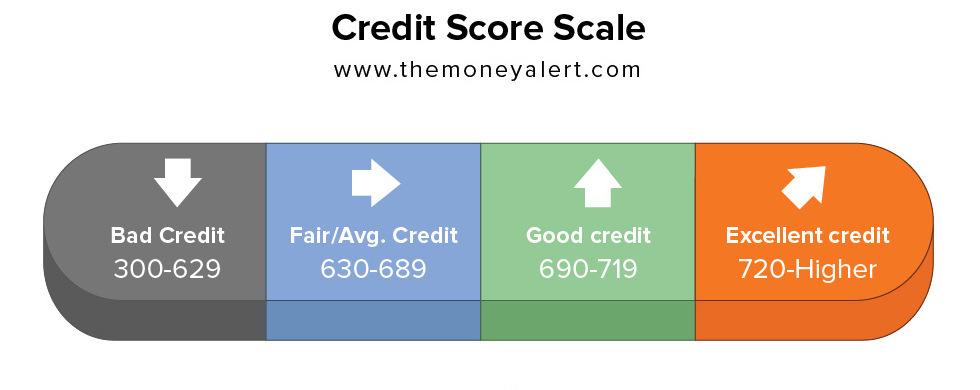

● 300 to 629: Bad credit

● 630 to 689: Fair or average credit

● 690 to 719: Good credit

● 720 and higher: Excellent credit

Keep in mind that what counts as a excellent, good, fair, or bad credit can differ between lenders as each has their own credit score cutoffs.

How Credit Scores Are Calculated

Credit scores are calculated using the information in your credit report. That information is supplied by the businesses you have a credit relationship with. Each month, your account details, including your current balance and payment status, are updated on your credit report. As your credit information changes, so does your credit score.

How you manage your credit accounts directly influences where your credit score falls on the credit score range. If you manage your accounts well – meaning you pay your bills on time and you don’t borrow more than you can afford to pay back – your credit score will fall on the higher end of the credit scoring range. On the other hand, mishandling your credit accounts will cause you to have a lower credit score on the lower end of the range.

In the United States, there are three major credit bureaus that collect credit information from your creditors and lenders. These bureaus are Equifax, Experian, and TransUnion. Each of these companies has their own separate database of information collected from various businesses and courts. These bureaus don’t share information with each other and some businesses may only report to one of the credit bureaus. Because of this, it’s possible for you to have different credit scores – all three of your credit reports won’t look the exact same. Each of your credit scores may fall in a different place on the credit score range.

You can check the information that the credit bureaus have on file for you for free once each year by going to AnnualCreditReport.com. You’ll be able to download a free version of your credit report from each of the major credit bureaus without having to enter your credit card information or subscribing to a credit report service.

Do You Have a Credit Score?

Not everyone has a credit score. The credit scoring calculation needs credit report information to generate a credit score for you. You need to have at least one account that’s been open and active for six months or more, you won’t have a credit score. If you’ve never had credit, recently opened your first credit account, or you’ve haven’t used your credit at all within the past six months, your credit report may not have enough recent information to calculate your credit score. Once your credit report has the right amount of information, a credit score can be generated for you.

Age and Average Credit Scores

Knowing the average credit score can help you gauge how you stack up against other consumers. In 2017, the average credit score was 700, which indicates the average consumer had good credit. Average credit scores were also different among various age groups according to Time Inc:

18-29: 652

30-39: 671

40-49: 685

50-59: 709

60+: 743

Based on these average credit scores, it apppears that your credit score improves as you age. It’s not directly because of age since age itself it not a factor in your credit score.

Age could be indirectly related to your credit score. The average age of your credit accounts considers both the age of your oldest credit account and the average age of al your accounts. This factor is 15% of your credit score. Having your accounts open for longer and minimizing newly opened accounts can help boost your credit score demonstrating that you have more experience with credit.

It can also be reasoned that as you get older, you become more responsible and have enough income to pay your bills and manage your debt amounts. Debt and payment history together make up 65% of your credit score. Managing these two areas can help you achieve a better credit rating.

Other Credit Score Ranges

While FICO is the most widely used credit scoring model, there are a few others created by the credit bureaus and the VantageScore. When lenders check your credit score, they may use one of these credit scores or another industry specific credit score.

● TransRisk New Account Credit Score: 300 to 850

● Experian National Equivalency Score: 360 to 840

● VantageScore 3: 300 to 850

● VantageScore 2.0: 501 to 990

● FICO 9 Credit Score: 300 to 850

● Equifax Credit Score: 250 to 925

● FICO NextGen Credit Score: 150 to 950

What is a Good Credit Score?

Having a good credit score is the goal of almost every consumer. That’s because there are a number of benefits of having a good credit score. Not only is it easier to have your applications approved, you can also qualify for lower interest rates, which means lower monthly payments and less money spent on interest costs. A good credit score helps you reach your goals of owning a home or buying a car by allowing you to get approved for the mortgage or auto loan. Your credit score comes into play whenever you apply for a credit card, an apartment, even when you get cell phone and internet service.

A good credit score comes from being responsible with your credit and other financial obligations. It means paying your bills on time each month, keeping your debt levels low, avoiding debt collections, and minimizing credit applications. On a credit score range of 300 to 850, a good credit score is generally above 690. An excellent credit score is above 720.

What is a Bad Credit Score?

It’s difficult to live with a bad credit score. Since many businesses use your credit score to decide whether to approve your application and to set the terms, a bad credit score makes it hard to accomplish even things as simple as having ulitilies turned on at a new apartment.

On a credit score range of 300 to 850, a bad credit score is below 629. If your credit score falls on the lower end of the credit score range, you may have many of your credit applications denied. When you are approved, you may have higher interest rates or even security deposits.

A bad credit score is the result of missing credit card and loan payments, defaulting on accounts, having one or more collections, or even having serious negative items like a foreclosure or repossession. You can recover from a bad credit score and by clearing up negative items, even if it means making a payment to bring the account back into good standing. When you review your credit report, look for negative items that are affecting your credit score. Working on these items and establishing a positive credit history will raise your credit score.

There are no guarantees when it comes to your credit score and applying for new credit accounts. Having a good credit score doesn’t automatically mean you’re approved and having a bad credit score doesn’t automatically mean you’re denied. The final decision is based on what you’re applying for and your other financial details like your income and debt. If you have an application denied because of your credit score, the lender is required to send you a copy of your credit score and the major factors affecting your credit score.

Checking Your Own Credit Score

Keeping tabs on your credit score can help you stay aware of where you are on the credit score range. You can use a free service like Credit Karma or Credit Sesame to check your credit score without having to enter your credit card number or subscribe. These free credit scores are for educational purposes and may not match what the lender sees when they check your credit. It will, however, give you an idea of whether you have good or bad credit and whether you need to work on your credit score.

Regardless of where you get your credit score, make sure you pay attention to the credit score range in addition to your three-digit credit score. Knowing the credit score range can give you perspective on your credit score, indicating whether your credit score is good or bad when it comes to credit scoring range.